February 2021 – today, nearly a year into our days of forced telecommuting and videoconferencing, the words ‘impact of COVID-19’ continue to ring in our ears. The hospitality industry has undoubtedly borne the brunt of this crisis, as many hotels across Europe continue to record single-digit occupancies, with average revenues per room down by nearly 70% in 2020. However, it would be hasty to presume that the long-term prospects of hospitality are all doom and gloom.

Newly released data from Cushman & Wakefield’s (C&W) Europe Hospitality MarketBeat 2020 reveals that contrary to what some may have expected, hotel transaction activity in Europe did not fall off the cliff during this crisis. While investment volume for the region declined considerably, by 63% compared to 2019, there was still over EUR 10 billion* of deals closed in 2020. With major transactions still taking place and deals continuing to be agreed upon amidst these times, it seems that investors remain optimistic about the medium to long-term prospects of the industry.

*Excludes acquisition of the Dutch vacation parks firm Roompot by KKR from PAI Partners for approximately EUR 1 billion

European Hotel Investment Market overview

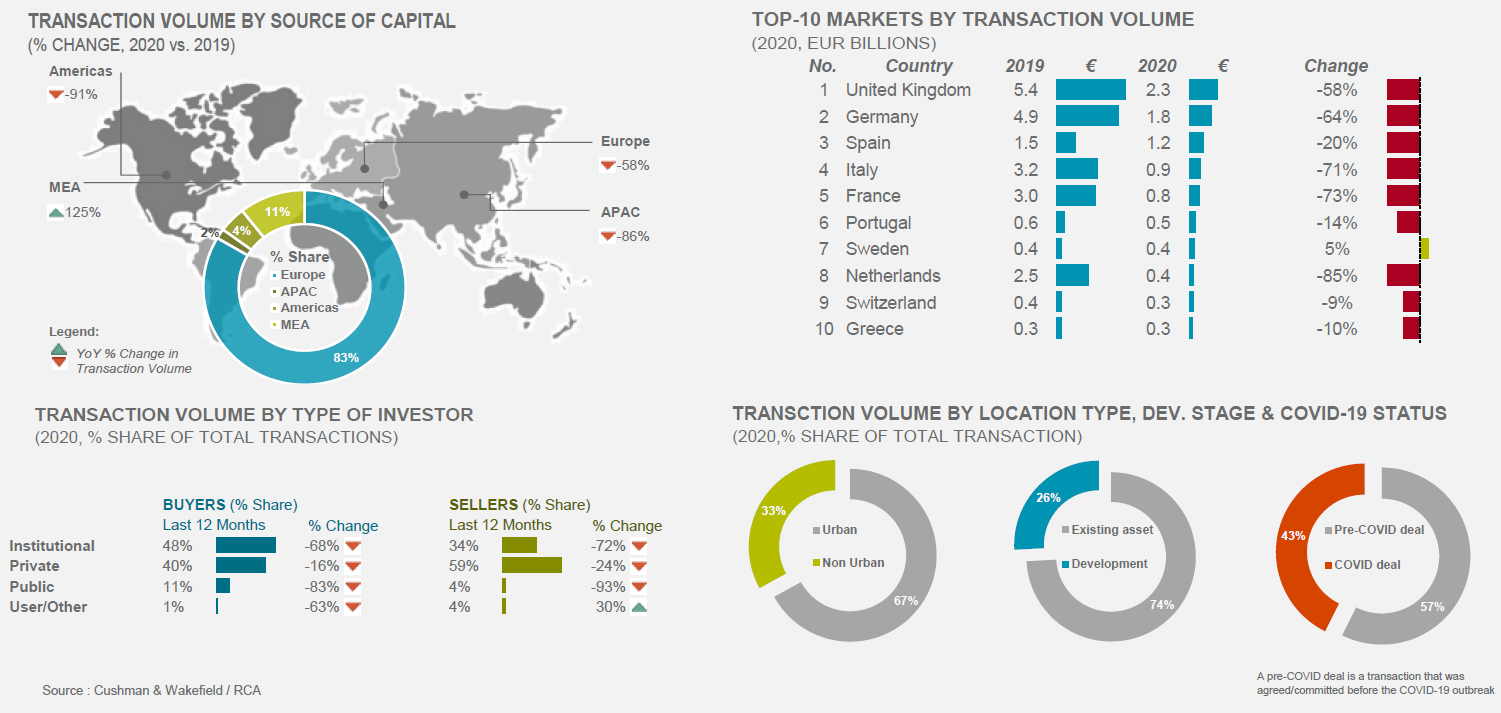

In 2020, the European hotel market recorded nearly 400 transactions, comprising about 48,000 rooms – of which almost 43% of deal volume was committed to after the pandemic outbreak.

Among the key deals done in 2020 include the sale of the iconic 136-key Ritz London to an unnamed Qatari investor and the acquisition of an 8-hotel portfolio across four key European countries for EUR 573 million by Covivio.

In particular, a few transaction characteristics have been observed in the last year:

- Investor Origin: Given the uncertainty caused by the pandemic, 2020 saw a marked increase in investors retreating to more familiar ground, with European investors accounting for a large majority of transaction volume in the region (83%).

- Investor Type: Institutional investors, who are better positioned to ride out such crises, led the transaction market with nearly half (48%) of total volume. These investors are typically better capitalised, more able to weather temporary troughs, and tend to have a longer-term investment strategy.

- Project Stage: Over a quarter (26%) of deal volume in 2020 was in development or conversion projects as opposed to operating assets, compared to 12% in 2019. Investing in projects that do not face the risk of requiring immediate capital injections to keep operations afloat is attractive for investors looking to buy assets which will be operational when the market returns. One example was the acquisition of the EDITION Madrid by Archer Hotel Capital for over EUR 220 million, which is expected to open in 2022.

- Location Type: Approximately 33% of transaction volume in 2020 was outside urban locations. However, when including only deals that were committed after the virus outbreak, the share of non-urban locations increased to over 41%. This may imply investors’ expectations of a quicker recovery and/or better long-term prospects for hotels driven by leisure demand that are typically located outside major cities. Unsurprisingly, there was a notable decline in acquisitions of airport hotels, down by 87%.

Rob Seabrook, Head of Hotel Transactions EMEA at C&W commented:

Despite the short-term challenges of the industry, over EUR 4.3 billion of transaction volume was committed to amid the pandemic in 2020 – this is a promising demonstration of continued investor interest in hotels. Investors who are familiar with the hotel market are especially confident in the long-term prospects for this sector, and the lower transaction activity in 2020 is in part due to the wait-and-see approach many investors have been adopting, rather than a waning of interest in hotels.

Excerpt from Cushman & Wakefield’s Marketbeat: Europe Hospitality 2020. Source: Cushman & Wakefield

Varied transaction performance across markets in Europe

Naturally, not all countries enjoyed the same spotlight of attention from investors. The UK and Germany saw a 58% and 64% fall in transaction volume respectively. However, they still retained the top spots, accounting for approximately 40% of total transaction volume in Europe, reaffirming their positions as two of the most active and liquid hotel markets in the region.

Among the least impacted major markets were Sweden, Switzerland, Greece, Portugal and Spain. Sweden in fact saw a slight increase in transaction activity, up by about 5% compared to 2019. Most notably, Greece saw one of its largest transactions by room count – investors Henderson Park and Hines join forces to acquire a 1,094-room, c. 67,000 sqm resort portfolio, comprising five seafront hotels across the popular Greek island of Crete; while Belterra Investment acquired the integrated 990-room Porto Carras Grand Resort on the Halkidiki central peninsula for over €200 million.

Porto Carras Grand Resort. Source: Porto Carras Grand Resort

There is a significant amount of capital that has been raised and is ready to be deployed on hotel transactions in Europe. Most of this money is searching for one thing that appears to be rare these days: distress. At this stage, we have seen very little of it. The pricing gap between sellers and buyers is still wide, but we see it narrowing and expect activity to pick up in the second half of 2021. There are a number of sizeable hotel portfolios currently on the market, especially in the Iberian Peninsula. Nonetheless, the investment market will likely only rebound when bank financing becomes more available.” - Frederic Le Fichoux, Head of Hotel Transactions, Continental Europe at C&W.

Looking ahead: Recovery for hotels and the investment market

Results for the European hotel investment market in 2020 show that investors remain cautiously optimistic, as they continue to be on the prowl for good deals. The 2008-2009 global financial crisis (GFC) saw a number of distressed hotel deals, with average hotel transaction prices in Europe down by 34% against the previous peak in 2007. However, these unprecedented times have also seen unprecedented efforts from governments to help the travel and tourism sector keep afloat, such as VAT cuts or co-paying wages. Similarly, banks have entered this crisis with a much healthier balance sheet, making them better placed to support businesses’ financial difficulties than during the GFC. Nonetheless, as the global pandemic and limited cash flows drag on far longer than anyone could have imagined, 2021 is likely to see more pricing adjustments and some distressed sellers.

Jonathan Hubbard, Head of Hospitality EMEA at Cushman & Wakefield, commented:

The hotel sector across Europe has been hit hard by COVID-19 lockdowns, which have understandably resulted in a sharp drop in investment volumes. However, the hotel industry is unique in that, for the most part, there is no viable virtual pivot for travel and tourism – there will always be a need for hotel accommodation. Investors recognise this, and their sentiment for the sector remains positive for the medium to long term. The continued transaction activity in 2020 and the number of deals we are seeing in the pipeline reflect this confidence.

Regardless of the uncertainty, there is one thing that remains certain. Travel restrictions have induced a temporary shift in travel patterns, with travellers switching from group to more individual travel; international to regional/domestic destinations – which above all, is an indication that the human desire to travel still persists, as people continue to find means and ways to take trips. Therefore, it is evident that the current investor confidence is not unfounded, and the overwhelming sentiment is that, “travel will come back”.

After all, there is no known vaccine for when the travel bug bites.

Download Cushman & Wakefield’s Europe Hospitality MarketBeat 2020