Insights into the various factors that have impacted Chinese tourists before and after the pandemic, and why the likelihood of a Chinese revenge tourism comeback is slim for the moment.

Chinese tourism: Pre and post-Covid

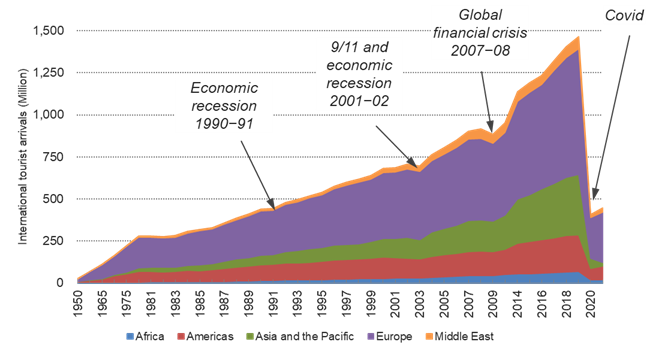

Global tourism in 2021 stood at 448 million tourist arrivals and US$637 billion expenditures, which was one-third of the pre-Covid level in 2019. To put it in perspective, the size of global tourism now is equivalent to that of 1990 in terms of tourist arrivals (Figure 1). This unprecedented recession has far eclipsed all impacts of the 1990−91 recession, 2001−02 terrorist attacks, and the 2007−08 global financial crisis combined.

Figure 1. Global tourism plunged during Covid. Source: UNWTO Tourism Barometer.

In fact, global tourism was likely to plateau out after 2019 even if Covid had not broken out. The Chinese market, which made up 10% of global tourist arrivals and 18% of expenditure, had shown signs of a slowdown due to the decreasing growth of Chinese economy. By the end of 2020, Hong Kong, which had been the largest destination for mainland Chinese and a gateway to many overseas destinations, saw Chinese tourist arrivals plummet by 94% compared to that of 2019. This was caused not only by the outbreak of the pandemic in early 2020 but also by the Hong Kong protest in mid-2019 that led to escalating political tensions and distrust between Hong Kong and the Chinese mainland for years to come.

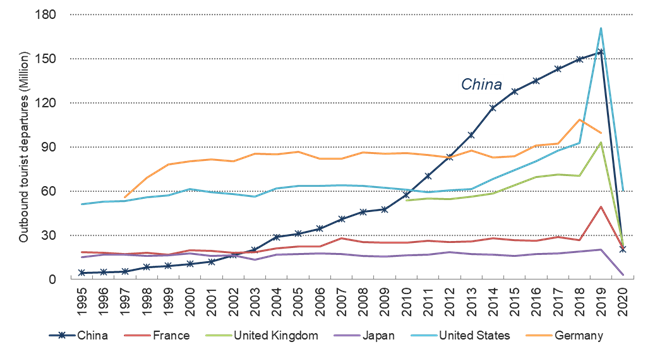

In retrospect, the recent decade of 2010−2020 was the golden period of global tourism, which was driven by Chinese outbound tourism. China overtook Germany in 2012 in terms of tourist departures and the U.S. in 2013 in terms of expenditures to be the largest tourist source market (Figures 2 and 3). All markets plunged during Covid. Since no emerging economy could supplant the Chinese market any time soon, many destinations are expecting the return of Chinese tourists when the Chinese government eventually abolished its zero-Covid policy. But will Chinese tourists make a revenge comeback?

Figure 2. Chinese outbound tourist departures. Source: UNWTO Tourism Barometer.

Figure 2. Chinese outbound tourist departures. Source: UNWTO Tourism Barometer.

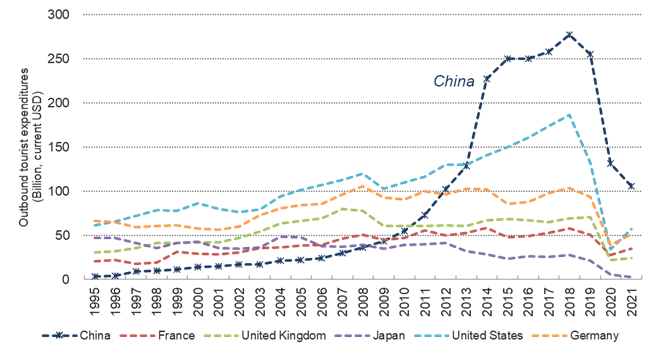

Figure 3. Chinese outbound tourist expenditures. Source: UNWTO Tourism Barometer.

Two fundamentals in tourism economy

To answer this question, we must acknowledge the fact that Covid exerted far severer global and persistent impacts than did any demand shocks since the 1990s. It undermined tourism demand in the long run. While tourism demand is highly elastic in the short run, sustaining tourism growth rests on the health of global economy and the increase in disposable income of consumers. This was of one of the reasons why Chinese outbound tourism was booming in 2010−2020, yet Covid has impaired this economic fundamental.

Figure 4. China GDP growth against selected economies. Source: World Bank. Note: Annual percentage growth rate of GDP at market prices based on constant local currency.

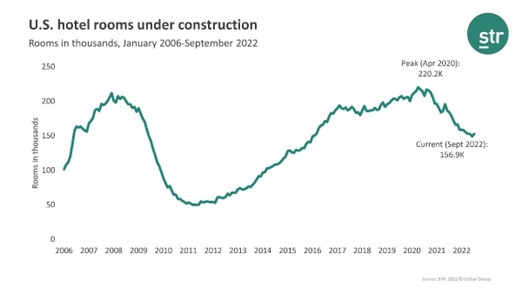

However, the biggest impediment to global tourism recovery lies at the extent to which supply can catch up with demand. When Europe scrapped its Covid polices in mid-2022, the industry was, and still is, struggling to resume and increase supply capacity, particularly in the airline industry. This included increasing flights, rescheduling air routes, and rehiring and training staff. However, this has been challenging because widespread layoffs in the industry during the pandemic dented people’s confidence in working in the tourism and hospitality industry. As a consequence, the industry is still grappling with severe labor shortages. Some businesses may hesitate to resume supply to full capacity (Figure 5), because they are not sure whether the increase in tourism demand can be sustained in order to make business profitable.

Figure 5. Hotel supply yet to recover in the U.S. Source: https://www.hospitalitynet.org/news/4113045.html#void (19 October 2022).

So, we have seen massive flight delays and cancellations as well as long queues at airports the past summer. The notorious flight cancellations of Southwestern Airlines in the U.S. in late December 2022 provoked widespread outrage of passengers, which ended up with a federal investigation of why. Due to insufficient supply and rising costs of many hospitality businesses, prices are inevitably being pushed up which in turn affects the recovery of tourism demand from many major markets. Note that these incidents and meltdowns only occurred at a regional level, in particular in the U.S. and Europe, where supply capacity is highly consolidated. The problem would become much more severe at the global level.

Uncertainties still remain

Since tourism is a preplanned and displaced consumption in an unusual environment, people are averse to uncertainty when traveling. The pandemic has not come to an end, with many mutations and variants of the virus spreading in different parts of the world. The WHO has no time frame to declare the end of Covid-19. These uncertainties are likely to cloud the recovery of the tourism industry and global economy in 2023.

After three years of lockdowns, the Chinese government abruptly overturned its draconian zero-Covid policy in early 2023. Not only was the shift of the policy drastic, but Chinese people seemed unprepared for the change. Such a Covid U-turn signifies the inconsistency and incoherence of China’s Covid policy that was supposed be predictable on a scientific basis. This is perhaps the largest uncertainty that Chinese consumers are facing.

Too early to make a comeback

The economic, social and geopolitical events, including the ongoing U.S.-China trade war started in 2018, the Hong Kong protest in 2019−20, and the Russia−Ukraine war in 2022, have caused tremendous distrust, discrimination and xenophobia. The politicization of the Covid policy and the origin of Covid has further exacerbated the lack of global cooperation and collaboration in combating the pandemic.

In response to the influx of Chinese tourists, many destination countries (the U.S., U.K, Australia, Japan and South Korea) started requiring a negative Covid test from Chinese tourists. This is more likely to be a gesture of preventing the spread of the virus. The discrimination, though, hurts tourism more than any other industries because tourism is based on an amicable host−guest relationship and can only thrive in a hospitable culture. Once conflict and protectionism displace cooperation and globalization, tourism and tourists will suffer.

Not only have these events affected consumers, but they have also affected suppliers. Despite the fact that the Covid policy is being relaxed across the globe, people may hesitate to travel and suppliers may be reluctant to increase supply. The Chinese market is more uncertain than other markets due to an incoherent Covid policy and a lack of confidence on behalf of Chinese consumers. Hence, I do not think there will be any revenge tourism recovery in 2023. I would rather hope to see a gradual recovery that can balance the needs of tourists and the supply of destinations. This would not only be good news for tourism but also for global economy as a whole.