Hotels can change brands (i.e. rebrand). An independent hotel may affiliate itself to a chain (or vice versa), or a branded hotel may change affiliation from one chain to another, or even within a chain. This choice can shape its identity, influence financial performance, and determine its long-term market positioning. However, while pivoting brands may offer a competitive advantage, it also comes with trade-offs.

With billions of dollars in brand contracts changing hands each year and more hotels switching affiliations than ever before, understanding the nuances involved in this process has never been more important.

A well-timed affiliation change can boost occupancy rates, strengthen brand equity, and unlock new revenue streams, while a poorly planned switch can disrupt operations and alienate loyal guests.

This post explores the key trends driving chain affiliation, the reasons hotels choose to affiliate or switch brands, the factors that influence these decisions, and the predictive models that can help industry leaders stay ahead.

Why Hotels Choose to Affiliate

Hotels choose to affiliate with major brands for a variety of reasons, but the core motivation often comes down to staying competitive. Chains can provide a level of support that can be difficult to replicate on a smaller scale.

For many owners, these benefits outweigh the costs, making brand affiliation a strategic choice for long-term success. Let’s inspect some reasons why hotels choose to affiliate.

Brand Recognition and Reputation

Affiliating with a well-established chain provides instant brand recognition and credibility, which can be a critical advantage in a crowded market, where a known name can influence traveler choice.

The built-in consumer trust that comes with affiliations like these reduces the marketing effort needed to attract first-time guests. This recognition extends beyond direct bookings, affecting third-party listings and overall market perception.

That said, some hotels do not rely on brand affiliation to achieve strong market positioning. Properties with exclusive locations, unique architecture, or rare amenities names often stand out without the backing of a major brand.

The same is true for heritage properties that have built loyalty through tradition and consistent quality. These often benefit from repeat customers, strong local reputations, and growing online booking channels, allowing them to compete without the overhead of franchise fees.

Standardized Operating Procedures

For many independent hotels, maintaining consistent quality can be a challenge. Affiliation with reputed chain hotels solves this by providing established operating standards that streamline daily management.

These procedures cover everything from front desk operations to housekeeping protocols and financial reporting, ensuring that each property meets a consistent standard.

For owners and investors, this kind of standardization offers clear benefits. It reduces training costs, minimizes the likelihood of expensive mistakes, and simplifies oversight, making it easier to manage multiple properties.

It also creates a more predictable guest experience, reinforcing the brand’s reputation for quality and reliability, which can be a powerful driver of repeat business.

Global Distribution Systems and Reservation Networks

Chain-affiliated hotels gain access to powerful global distribution systems (GDS) and centralized reservation networks. These platforms connect properties to a vast network of travel agents, corporate bookers, and online travel agencies, significantly expanding their reach.

This technological advantage allows hotels to capture demand from international travelers and major corporate accounts, which might be challenging for independent operators. It also simplifies revenue management through automated inventory updates and real-time pricing adjustments.

Training Programs and Resources

Most chains offer comprehensive training and support programs for staff at all levels. These programs are designed to ensure that employees can deliver the brand’s signature guest experience, regardless of location.

This involves access to cutting-edge management tools, leadership development programs, and ongoing professional education, helping to reduce turnover and boost staff morale.

An influx of resources like these can work wonders for independent hotels struggling to standardize their guest experience.

Procurement Advantages

Affiliation provides significant purchasing power, allowing hotels to negotiate better rates on everything from linens to technology. Centralized procurement not only cuts costs but also ensures consistency in guest-facing items like bedding, toiletries, and in-room amenities.

This advantage extends to services as well, with chains often securing bulk rates for digital marketing, insurance, and maintenance contracts, further improving the bottom line.

Loyalty Programs

Affiliation grants access to extensive loyalty programs, which can be powerful drivers of repeat business. These programs reward frequent travelers with points, perks, and exclusive benefits, encouraging brand loyalty and increasing lifetime customer value.

Moreover, a well-structured loyalty program generates valuable guest data, enabling more personalized marketing and targeted promotions, which can significantly boost revenue.

Why Hotels Leave Chains

There’s two sides to every coin. While affiliating with a major brand can offer numerous benefits, it also comes with significant financial commitments. Franchise fees, royalties, and marketing contributions can eat into margins, making it harder for hotel owners to achieve their financial goals.

These costs can add up over time, as brands expand their marketing efforts and update operational standards. For some hotels, particularly those with stable demand and loyal customer bases, these fees can feel like an unnecessary drain on resources.

The long-term nature of many franchise agreements can also be restrictive, locking owners into a relationship that may no longer align with their strategic goals.

Beyond financial concerns, many hotels choose independence for the freedom it provides. Some owners prefer to control every aspect of their property, from room design to guest experience, without the constraints of brand standards.

Others may have a niche appeal that sets them apart from the cookie-cutter approach of larger chains. In these cases, the ability to respond quickly to local market trends and personalize the guest experience can be a significant advantage.

For hotels with a strong, well-established brand of their own, breaking free from a larger chain can be a step toward building a more authentic and differentiated guest experience.

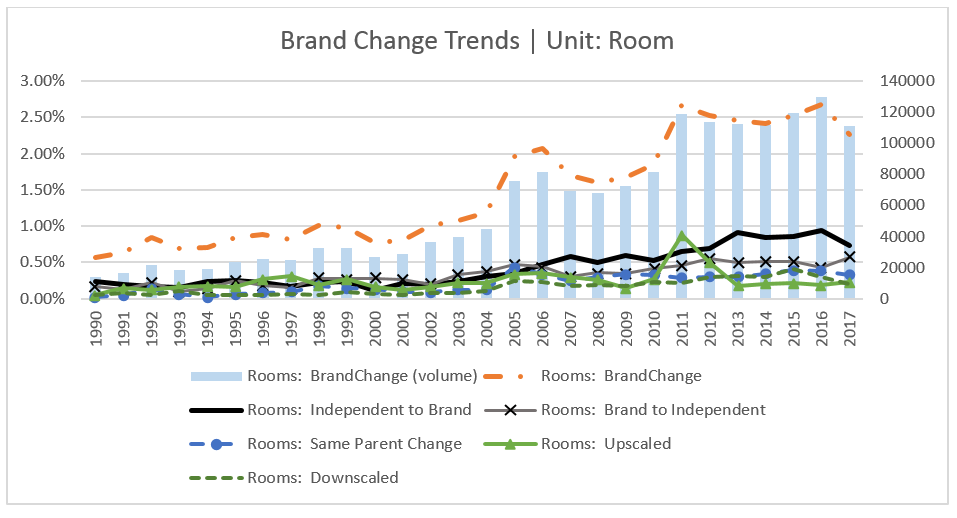

The Rise of Chain-Switching and Rebranding

Percentage of rooms rebranding over the total, between 1990 and 2017 | Prashant Das, PhD & Isabella Blengini, PhD

For some hotels, the decision to break free from a major chain is only part of the story. Many owners and investors are now opting to reposition their properties within the branded ecosystem, shifting from one chain to another in pursuit of a better strategic fit.

This rise in brand fluidity is partly fueled by the growing popularity of soft brands and conversion-focused models, which offer many of the advantages of large networks without the rigidity of traditional franchises.

The pace of hotels switching from one chain to another now exceeds the growth in independent hotels joining major brands. In fact, chain-to-chain mergers are growing at around 9% annually—slightly ahead of the 8% growth rate among independents affiliating for the first time.

To put this in perspective, overall hotel supply has grown by only 2% annually. That gap highlights a clear trend: rebranding activity is significantly outpacing new development.

In 2018 alone, we estimate that nearly $500 million worth of brand contracts shifted between chains. With this level of value in motion each year, it’s increasingly important for asset managers and consultants to anticipate when a hotel is likely to rebrand.

Together, these trends highlight the increasing importance of strategic brand alignment in the hotel industry, where the right affiliation can mean the difference between a thriving property and one that struggles to keep pace.

Independent-to-Chain Conversion

One of the most striking trends has been the rapid growth in independent hotels affiliating with major brands.

According to our study, from just 57 hotels (4,445 rooms) in 1992, this segment expanded to 371 hotels (36,074 rooms) by 2017—a roughly 7-8 fold increase, representing about 8% annual growth.

This reflects the appeal of established brand support, global distribution, and loyalty programs, which can significantly boost occupancy rates and financial performance for properties willing to give up their independent status.

Chain-to-Independent Conversion

While less common, the opposite trend also exists. We found that chain-affiliated hotels going independent grew from 42 hotels (5,882 rooms) in 1992 to 280 hotels (28,002 rooms) in 2017.

This movement remains smaller in scale, often driven by owners seeking greater operational flexibility or a desire to carve out a unique identity in the market.

These hotels may prioritize creative freedom and local connections, or a unique identity over the more structured, standardized experience of a chain brand.

Drivers of Hotel Chain Affiliation

At first glance, rebranding may appear to be a private decision—one that depends on internal, asset-level factors that are hard to observe externally. If that’s true, then it would seem almost impossible for outsiders to reliably predict when or why a hotel might rebrand.

But hotel decision-making doesn't occur in a vacuum. In competitive markets, rebranding choices are heavily influenced by broader macroeconomic trends, and many observable characteristics, such as a hotel’s size, type, age, and location.

With this in mind, we examined rebranding trends across 66,000 U.S.-based hotels using data from STR. Our aim was to model the likelihood of rebranding using only publicly available information about the hotel and its market context.

Our investigation set out to determine whether certain hotels are inherently more likely to rebrand based purely on their observable physical, geographic, and contractual characteristics.

The results confirmed our expectations: a substantial portion of rebranding activity can be attributed directly to the traits of individual assets, with broader market trends explaining much of the remainder.

Notably, shifts in financial market sentiment (both optimism and pessimism) appeared to significantly influence affiliation changes. In the course of our analysis, several unexpected and valuable insights also surfaced.

Historical Behavior

One of the more interesting findings was the role of historical behavior. A hotel’s history of prior rebranding has a nuanced effect on future brand switching.

While a few early rebranding tend to increase the likelihood of subsequent changes, potentially by normalizing the process or signaling strategic agility, this trend doesn’t continue indefinitely.

Beyond a certain threshold, additional rebranding history actually lowers the probability of further changes. This suggests that while rebranding can build momentum initially, there may be diminishing returns or reputational fatigue that ultimately discourages additional brand shifts.

Property-Specific Characteristics

Certain structural and operational characteristics strongly influence a hotel’s likelihood of rebranding. This may reflect a stronger embedded identity, operational inertia, or reduced viability of repositioning.

Additionally, all-suite hotels showed a lower propensity for rebranding, possibly because of their niche appeal or an already loyal customer base that could be disrupted by affiliation changes.

Geographic placement also plays a key role. Hotels situated along interstate corridors are significantly more likely to rebrand than those located near airports, while other location types did not exhibit consistent rebranding patterns.

Luxury and mid-scale hotels emerged as the most active segments to rebrand, and larger or taller hotels were found to be more prone to changing brand affiliations, potentially because of the scale of investment required and the commercial impact such moves can yield.

Market and Economic Drivers

Macroeconomic factors also proved to be strong predictors of brand affiliation changes. We observed that a steeper yield curve, commonly interpreted as a sign of economic optimism, correlated with increased rebranding activity.

In this context, the term spread appears to act as a signal for future expansion, motivating both owners and chains to pursue new branding opportunities in anticipation of growth.

Beyond interest rates, broader market conditions such as commercial real estate performance and equity market volatility were linked to rebranding trends. Robust real estate markets and spikes in stock market volatility both tended to precede higher rates of rebranding.

Additionally, hotel markets experiencing stronger income flows and faster value appreciation saw more brand switching, suggesting that high-growth environments encourage more aggressive repositioning strategies.

Strategic Motivations

Digging deeper into the data, we uncovered more subtle behavioral patterns tied to specific types of rebranding. Older hotels, for example, were less likely to shift from independent status to an affiliation or to switch brands altogether.

However, these same properties showed a greater tendency to become independent or to reposition within the same brand family.

This indicates that while older hotels may resist bold external changes, they are still open to strategic realignments that preserve continuity while adapting to new market demands.

Larger properties are less likely to pursue up-scaling but more likely to downscale, perhaps due to operational constraints or market positioning. In contrast, boutique hotels often lean toward up-scaling.

Resorts stood out as being relatively resistant to class-level rebranding, possibly because of their strong identity or fixed market positioning.

Somewhat counterintuitively, we also found that periods of high market returns and volatility were associated with increased down-scaling—an unexpected reaction in what are usually optimistic conditions.

A Tool For Prediction

To make our findings usable in practice, we developed a simplified parametric model with fewer variables, suitable for industry professionals. Based on this, we created an Excel-based tool, available via the EHL Real Estate Finance and Economics (REFE) Institute website.

This tool predicts how long a brand is likely to remain with a hotel based on basic details. For instance, consider a 300-room, single-story luxury hotel in the Mid-East that has switched brands three times. The tool estimates a 13-year median duration before its next rebranding.

For even more precise forecasts, we recommend developing locally specific models that capture a broader range of variables.

The Path Forward

The hospitality business is undergoing a profound shift, where chain-switching and rebranding reflect a broader embrace of agility and innovation.

In the U.S., 32% of hotels have been rebranded at least once, with some switching brands up to seven times. This movement represents nearly half a billion dollars in annual brand contract transfers, making rebranding a critical factor for hotel strategists.

As hotels evolve into data-driven, adaptable assets, owners and investors can leverage technology and macroeconomic insights to anticipate guest preferences and market dynamics with remarkable precision.

This strategic flexibility, whether through soft brands, independence, or chain realignment, positions properties to redefine guest experiences in a hyper-connected era.

By embracing this approach, industry leaders can transform their hotels into vibrant hubs of innovation, not just adapting to the future of travel but actively shaping it.

Citation

Blengini, I., & Das, P. (2020). Why a New Name? The Role of Asset Characteristics and Broad Market Trends in Predicting Brand Affiliation Change in Hotels. Cornell Hospitality Quarterly. doi.org/10.1177/1938965520924648

Special thanks to Steve Hood and Duane Vinson (STR/CoStar Global) for data support, Remy Rein for insights on hotel brand dynamics, and Andrew Brenner for copyediting.