Branded residences are luxury homes associated with well-known brands that offer residents hotel-like services and convenience. Rising demand is coming from experience-driven individuals seeking unique and exclusive living.

Have you ever had a hotel stay so lovely you did not want to leave? The world's luxury brands are making it possible for you to stay. The branded residential sector has grown rapidly since its inception in the 1980s, and an increasing number of luxury brands are flocking to this model. Investors and developers are benefiting from high premiums compared to unbranded properties.

This article explains what branded residences are, what kind of opportunities and challenges they offer investors and developers, and the future trends shaping this fast-growing sector.

What Are Branded Residences?

Branded residences are residential properties tied to a brand. They allow residents to live out the lifestyles of their favorite brands, with the main value proposition being an unparalleled service level – the ease of a hotel-like living experience extended to everyday life. These signature-branded environments are in prime locations, hosting beautiful design and architecture.

Furthermore, they adapt to the modern individual’s wish for blending work, living, and leisure, and allow for delegating everyday tasks to be managed by the brand. Amenities can include concierge, housekeeping, restaurants, and wellness offerings.

Luxury hotel brands dominate the sector, with names such as Rosewood, Mandarin Oriental, and Aman offering lovers of the brand a living experience marked by their signature service standards. They are turnkey solutions for buyers, where every detail, from the architecture and design to furniture, reflects the brand’s values and prestige.

While branded residences are operated mainly by luxury brands, midscale, upscale, and upper-upscale segments are also represented. Luxury itself is evolving, with trends pointing to more stripped-down interpretations with high emphasis on experience-enhancing service.

However, hotel brands are not the only ones rethinking living. A growing proportion of branded residential properties are by non-hotel brands, from cars (Porsche, Bentley, Aston Martin) to fashion (Elie Saab, LVMH), and F&B (Nobu, Cipriani).

In 2025, there are over 700 branded residences globally, with an equal number of projects under development. Residential hospitality is experiencing a prolonged growth boom for a good reason. Investors and operators alike are seeing the added value brands bring to real estate, with soaring price premiums and long-term value retention and appreciation.

Why Branded Residences Command Premium Prices for Investors

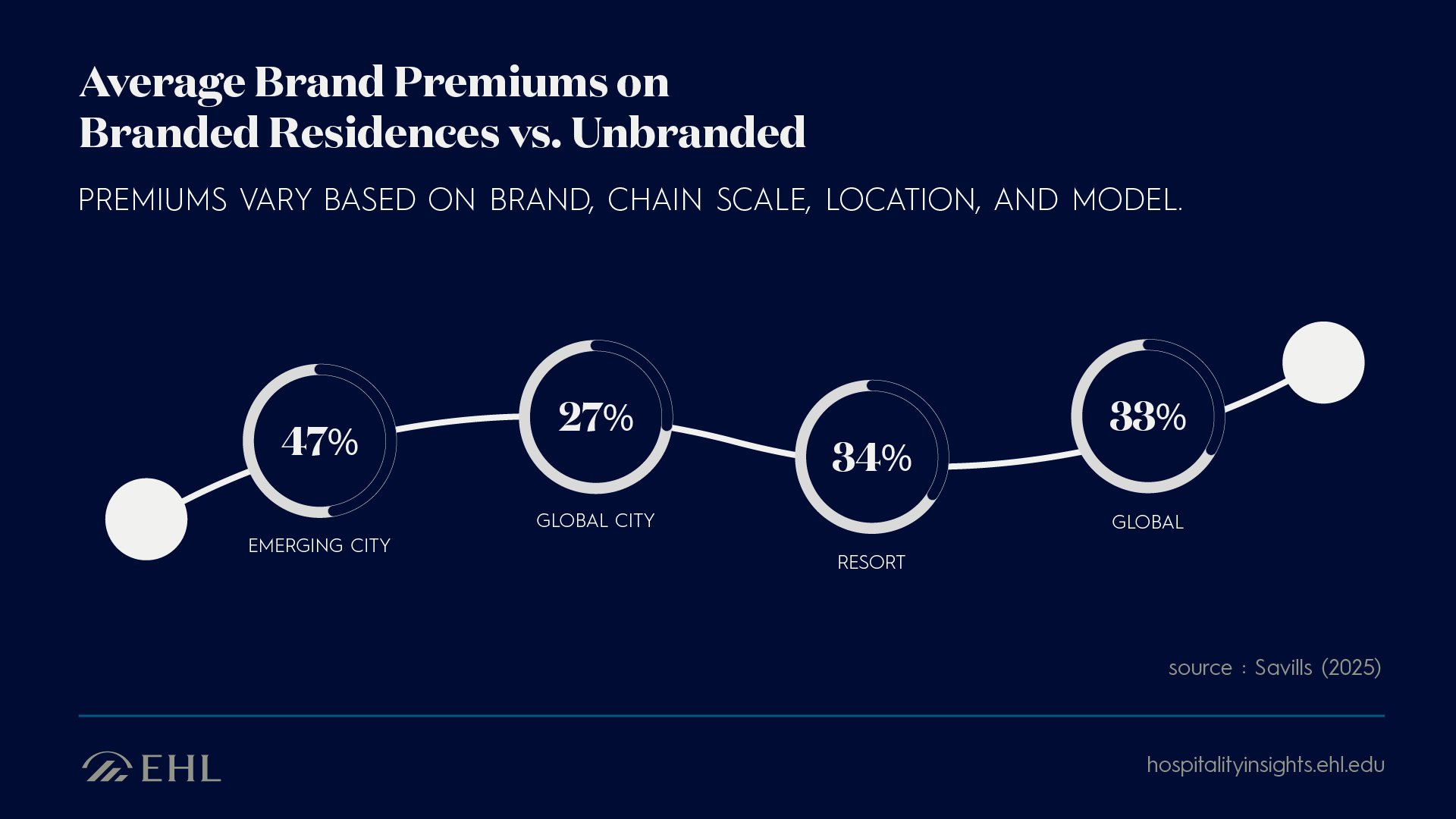

The price tags of branded residences have inflated price tags compared to similar, unbranded properties. According to Savills, branded residences command the following average premiums over comparable unbranded properties.

- Global average: 33%

- Resort destinations: 34%

- Global cities: 27%

- Emerging cities: 47%

These averages vary based on location and segment. For instance, the price premiums in global cities are slightly suppressed compared to the sector average due to market dynamics and higher competition. Emerging cities see the highest markups. In Dubai, the most active market of the whole sector, select residences have seen premiums of even 90%.

Alt text: Chart showing branded residence price premiums by market: 47% in emerging cities, 34% in resorts, 27% in global cities, 33% global average. Source: Savills.

As we can see, adding a renowned name greatly inflates a residential property's price. But what is this perceived additional value from the brand based on?

Luxury branding builds a sense of exclusivity, and people are willing to pay a premium to live the lifestyle their favorite brand promises. In fact, buyers are often propelled by a sense of affinity and loyalty, having had previous positive interactions with the brand.

Furthermore, branded residences are more resilient in economic downturns and retain more value than comparable properties that are not affiliated with a brand.

However, the premium pricing advantage is only realized when the service level and residential experience truly reflect the brand promise. This requires operational excellence and first-rate hospitality management.

Branded Residences Market Growth and Demand Trends

The sector has grown 180% in the last decade, with ongoing growth. The compound annual growth rate has been in double digits between 11% and 17%, and the pipeline suggests this is a continuing trend. The supply of branded residences is expected to double by 2030.

This supply growth is a response to continued demand for experiential and branded living, driven by two main factors: a shift towards experiences and the growing number of individuals who can afford this product.

Demand Driven by a Shift Towards Experiences

The dynamics of the economy have undergone a change, where experiences and immersion are valued over physical products–also called the experience economy. Branded residences are in many ways experiential products, with their value largely dependent on the ‘vibe’ created by the brand. This makes them an increasingly attractive way of living.

More Affluence, More Buyers

Furthermore, more people are affluent enough to access such offerings. The growing global economy is creating more (ultra) high-net-worth individuals, and the population is expected to grow by 38% by 2028.

Top Branded Residence Companies: Hotel and Non-Hotel Brand Leaders

Leading Hotel Brands in the Sector

Regarding parent companies, the market leader is Marriott International, which holds the same title when it comes to the number of hotel properties in the world. The company hosts an impressive portfolio of luxury brands, including the Ritz-Carlton, St Regis, and W Hotels, which all operate private residences under their name.

Marriott is followed by Accor and sector pioneer Four Seasons in the number of developments completed and underway.

Lifestyle and Automotive Brands Expanding into Real Estate

A wide array of non-hotel brands–including haute fashion houses, fine jewelers, and car brands– are expanding into residential real estate. The fastest-growing branded residences portfolio is that of Turin-based automotive designer Pininfarina. The company has 30 projects in its pipeline, with an emphasis on South America.

Why would an automotive brand put so much ammunition into branded residences? Pininfarina’s sentiment of expanding its lifestyle strategy to a 360-degree experience is the rationale behind many non-hotel brands entering the sector. Expanding into real estate offers diversification and functions as yet another canvas for the brand’s storytelling and values.

Pininfarina, for instance, wants to convey beauty and technology, two elements central to the brand, through carefully crafted ‘environments’.

These mixed-use opportunities are critical strategic tools for brands that want to expand and diversify their global portfolios.

Branded Residence Models Explained

As for the real estate asset itself, brands often do not have their skin in the game, even though it informs every phase of the development of a branded residential property. Instead, they operate and manage the property under a management agreement and, in exchange, receive management fees of 2-3% of property value and rental income in properties with a rental program.

There are two main models for branded residences, each with its pros and cons. Branded residences can either be adjacent to a hotel (in the same building or close to a hotel) or standalone.

Integrated Hotel-Residence Model

Most branded residential properties are integrated or directly near a hotel of the same brand. These properties benefit from reduced costs and operational overlap. Revenue is generated from unit sales and service fees from access to the hotel’s amenities.

Furthermore, hotel investments that are known for being risky can become more attractive with the added component of private residences. The added revenue stream of service fees and enhanced ancillary income from residents using the hotel’s F&B, spa, and wellness services can strengthen a hotel investment case.

However, hosting guests and residents under the same roof adds complexity. Brands need to distinguish the experience of the hotel guest and the resident, making sure the expectations of both are met.

That said, when synergies are realized, mixed-use developments with hotels and residences offer strong investment opportunities that bypass the many concerns related to hotel investments alone.

Standalone Branded Residences

Not all branded residences are located alongside their hotel counterparts—standalone residential properties are increasingly under development. While they still offer the same branded living experience and signature service levels, standalone properties naturally distinguish the residential lifestyle from the hotel guest experience.

The main benefit of operating standalone residences is simplicity. Due to not sharing infrastructure with a hotel, there is lower operational complexity. Furthermore, the range of residential services may be narrow or more curated, allowing for leaner operational costs.

On the other hand, the standalone properties miss out on the synergy benefits. The price markup must be justified because they are not directly connected to a hotel.

Still, standalone properties represent a growing portion of brands’ development pipelines. For instance, while these properties represent only 10% of the total branded residences supply, about 25% of Marriott’s upcoming developments are standalone. In some ways, they are more exclusive and resident-centric and can be highly successful with the correct location and brand.

Case in point: The Whiteley in London will have 139 unique private residences operated by Six Senses, which is known for its sustainability, world-class wellness offerings, and service level. The residences are adjacent to a hotel in the same building. Amenities include an indoor swimming pool, which is entirely exclusive to residents, and access to hotel services is only a phone call away. There is a focus on clear separation between residents and hotel guests. The development also taps into another trend on the rise, private members clubs, with residents gaining access to Six Senses Place, which offers social and co-working spaces and restaurants. The location is prime, and the redevelopment of the historic building (a former Waldorf Astoria) is a sustainable initiative with the adaptive reuse model.

Investment Opportunities and Risks in Branded Residences

Branded residences are unique ecosystems for living and working that are increasingly in demand. Catering to consumers’ call for exclusivity and branded lifestyles, residential hospitality presents opportunities to investors and developers. However, there are also risks that come with the specificities of the sector.

Benefits of Branded Residences for Developers

The real estate market is crowded. Branded residential hospitality is a resilient asset class that differentiates from other products and caters to real market demand, translating to long-term value and appeal.

Revenue Potential Through Pre-Sales

Branded residences are financially attractive for investors and developers due to the possibility of pre-sales. Developers often sell units before completion–sometimes selling out based on pre-marketing materials alone–and deposits can reach up to 70% before handover. This gives developments early cash flows and a faster payback period, reducing financial exposure.

Improved Access to Financing

Because of economic uncertainty, financing pure hotel projects has become more difficult. However, successful pre-sales can help with lender confidence, and developers may have to rely less on debt in the first place.

Key Challenges in Branded Residential Developments

Branded residences promise big wins for brands and investors alike, but there are some considerations that come with this unique asset class. Below are the most notable challenges developers face.

Misalignment Between Ownership and Brand Agreements

Firstly, timescale discrepancies can pose a significant risk to asset value. When buyers purchase a branded residential property, it is generally a freehold. However, management agreements with brands tend to be shorter-term (around 30 years for luxury brands), which means that, in theory, the brand of a residence can change if the original contract is not renewed.

This can create a conflict between the buyer and the developer: the buyer purchases a property under a specific brand, and the property's value can be affected even if it is rebranded under an “interchangeable” brand.

Challenges for Non-Hospitality Brands

Especially non-hotel brands are facing the challenge of communicating brand value. It is not enough to slap a brand on a residential property and call it a day. Projects must be thought out to the smallest detail, starting from the pre-design phase, to justify the premiums and live up to the brand promise.

Non-hotel brands are at a disadvantage compared to luxury hotels, as they do not have a heritage of high service level and property management. Additionally, hotel residences benefit from the brand’s investments in food and beverage, services, and wellness. In contrast, non-hospitality companies may have to spend significant resources crafting their service concepts.

Brand Reputational Risk

It goes without saying that if the brand’s image is damaged, it can significantly impact the property’s worth.

Nonetheless, these risks can be mitigated by having contract clauses that protect the asset's value and ensuring brand standards inform each development phase, from architecture and design to sales materials.

Looking Forward: Branded Residences Trends

With fast growth comes shifting dynamics. Here are the key trends in the branded residences sector, hinting at some great investment opportunities and what is expected of brands as the sector matures.

Branded Residences in Emerging Markets

Emerging destinations are leading development, with the Asia Pacific soon representing as large a market share as North America. Other notable markets delivering outsized premiums are Malaysia, Vietnam, and India.

Growth comes from strengthened GDPs and an increase in wealthy individuals, with this demographic generally being younger and more brand-conscious than in mature markets.

Midscale and Non-Hotel Branded Residences Growth

A growing share of the market is represented by non-luxury brands. Midscale and upscale segments grew by 24% in 2024 alone. Beyond ultra-luxury, branded residences are increasingly regarded as viable investment opportunities providing consistent, brand-associated living experiences.

Similarly, non-hospitality lifestyle brands are taking up more space in the sector, with their global share soon reaching 21%. These companies are looking to leverage real estate to be an extension of their brand promise and identity.

Tech and Wellness Innovation

With the influx of new supply, brands must find a way to differentiate their offerings to stand out and attract buyers. Experts note that there is still room for innovation, especially with tech and wellness-focused experiences.

Forward-thinking brands are responding by tackling all lifestyle needs imaginable. For instance, The Standard Residences in Miami offers unexpected amenities such as a karaoke bar and meditation studio.

Why Branded Residences are a Smart Investment for the Future

Branded residences are a compelling asset that combines residential real estate with a lifestyle brand. The properties are resilient and differentiated in a crowded market and benefit all stakeholders from developers to operators. For residents, they deliver truly exclusive living that reflects the prestige and emotional connection associated with their favorite brands–perhaps, the ultimate immersive hospitality experience.

As non-hospitality brands continue to enter the space, demand is expanding beyond the traditional ultra-luxury segment. While the sector has challenges, those who approach branded residences with attention to the brand promise can expect long-term value creation.